“Dance your cares away…

…worries for another day.”

A great mantra from the Fraggles and one which someone like me, who catastrophises daily about all manner of things, should probably take on board[1].

Let’s all be more Fraggle.

But, only to a point.

You see, when it comes to tax and investment planning that approach might have some drawbacks.

And with that, I return to the ongoing story of Magic Beans…

…0r the magic use of magic Bills of Exchange (“BOE”).

As anyone who is anyone knows, in Ghostbusters [2] , there was a famous warning against crossing the proton streams from their proton packs as they might “cause a chain reaction, which may lead to total protonic reversal”.

Now, I am not sure what a protonic reversal is – but this is precisely what we might get if we combine:

1. The Magic Beans; and

2. the umbrella company industry.

Yes, you’ve read that correctly.

Fraggle Rock Limited

So, let us say there is a company which is marketing BOEs as a method for, inter alia, settling tax liabilities such as VAT, PAYE and SDLT.

A firm like the one that I spoke about in my original article on Magic Beans.

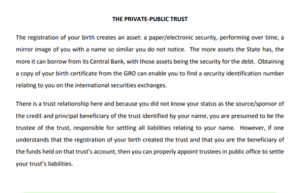

As a reminder, these BOEs are drawn on a magic trust created at birth by the Government. But it is a magic trust you never get told about by the Establishment. In fact, they will probably resist and deny its magic-y existence even when you are left alone in less magic-y circumstances, in Court, trying to explain what the heck has happened.

To maintain the theme, I’m going call that business Fraggle Rock Limited.

One of the stakeholders of this totally imaginary [3] company appears to be a fully-fledged subscriber to the Sovereign Citizen ideology.

Let’s say his name is Uncle Travelling Matt.

We can guess he is a subscriber to the magic hat brigade because he has added an odd symbol to his name by deed poll. He now goes under the name, Uncle-Travelling Matt.

Eh?

Judge JD Rooke [4] in an Albertan Kings Bench case in Canada (Meads v Meads [5]) set out a detailed overview of Sovereign Citizen / Freeman litigants (the Judge refers to these as OPCA [6] litigants) which is well worth a read if encountered by this type of character. The Judge said this:

Why add random characters to a name? Here’s the Judge’s explanation:

The judgement referred to above is an excellent distillation of the characteristics and arguments of so-called Sovereign Citizens / Freemen / OPCA believers.

Of course, the hyphen might be a coincidence… and he just likes Terry-Thomas.

So, what’s going on with magic beans?

Broadly speaking, we are told that these magic BOEs can be used to settle liabilities of all kind – including taxes.

But aren’t BOEs simply a posh name for cheques?

Well, let me tell you a story. Actually, I’ll let TreasuryDirect, a US Gov website, tell you the ‘story’ which is as follows:

When the United States went off the gold standard in 1933, the federal government somehow went bankrupt.

With the help of the Federal Reserve Bank, the government converted the bodies of its citizens into capital value, supposedly by trading the birth certificates of U.S. citizens on the open market.

After following a complicated process of filing UCC documents with either the Secretary of State of the person’s residence or another state that will accept the filings, each citizen is entitled to redeem his or her “value” by filling out a sight draft drawn on their (non-existent) TreasuryDirect account.

The scheme asserts that each citizen’s Social Security Number is also his or her account number.

As a part of the scheme, participants also file false IRS Forms 8300 and Currency Transaction Reports in the name of law enforcement officials and other individuals they seek to harass.With early and vigorous prosecution by the Justice Department on bogus Sight Draft cases, we have begun to see Bills of Exchange taking their place.

This change occurred on or around January 2001.

All these Bills of Exchange drawn on the U.S. Treasury are worthless.

All the same issues and background materials applicable to Sight Drafts also apply to Bills of Exchange.

This is the same fraud under another name.

But that’s the US. They have maple syrup on bacon. It couldn’t happen in the UK?

Well, the Magic Beans scheme is essentially the UK version, with one or two tweaks.

Let’s hear about the magic trust shall we [6]:

So, the story is slightly different. It is not government bankruptcy that created the trust. Instead, in this version of the fairytale, it is your birth that creates the magic fund that you and your fellow Red-Pillers can dip in and out of(!)

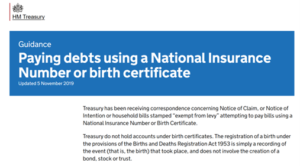

Lo and behold, the Treasury dismissed this [7] barmy idea back in 2019:

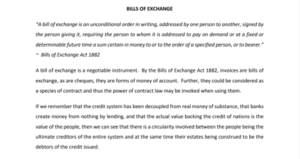

Next, we get the spiel on bills of exchange [8]:

But, hold your horses.

We then have some legal authority for this plan thrown in our faces. From the indomitable Lord Denning no less [9]:

We can’t argue with Denning, surely.

But it’s difficult to see how a quote could be taken any more out of context than this.

The quote is used to demonstrate some judicial authority that the ‘cheque’ is to be treated as if it is cash. As such, the recipient must accept it in settlement of the debt.

But, of course, this isn’t what he was saying.

In fact, it is averred, Lord Denning was saying precisely the opposite.

What he was saying in that passage is that if a debtor provides a bill of exchange or a promissory note to a creditor, it is binding on the debtor. In other words, the debtor (person making out the cheque) must honour the cheque unless there is a good reason why not.

Importantly, a bill of exchange will only extinguish an existing debt if the creditor agrees with that mechanism of payment. Of course, a creditor is always entitled to insist on payment in legal tender.

A creditor need no more accept a bill of exchange than he or she must accept a payment in magic beans.

So, what does the promoter say about the position if the creditor refuses [10]?

Well that’s handy. If they refuse it, they are accepting it.

Check mate, creditor.

Of course, this is bobbins.

Indeed, this is something that was considered by the Financial Ombudsman in a complaint by mortgage holders who tried to settle a mortgage with bills of exchange from a bank, which wasn’t really a bank, called WeRe Bank. Additionally, the FCA issued an alert against WeRe Bank back in 2015[11].

As per the footnotes, these documents were provided to me by a person who got the whole Fraggle Rock Limited pitch. The documents were really agricultural. These might be a little slicker now. After all, their website has markedly improved since my first article. Probably those Doozers at work.

Back to tax?

So, what has this got to do with tax?

As I said in my first article on the Beans, I came across this preposterous proposition when one of Fraggle Rock’s employees – we’ll call him Boober – was shilling it to one of my clients.

In this case, he was a property developer and was quite interested in pretty much anything that might ‘help’ him pay his SDLT liability.

In the old days, when SDLT schemes existed, there was usually a series of transactions where, for one reason or another, one of those transactions led to a saving. There was some kind of attempt at a technical argument – of varying degrees of merit.

However, Boober proposed no such chicanery. The advice was simple. Create a BOE – that draws on this magic and secret fund held by the treasury – and use it to pay your tax liability.

If they don’t respond… they’ve accepted.

If they reject it, then even better!

What’s the issue?

So, what is the actual harm being done by our magic, tin foil hatted purveyors of magic beans?

I am not sure that there is any tax-related fraud (against the Revenue [12]) here because:

- It is so ludicrous that HMRC will be too busy laughing their civil service issued socks off; and

- It seems that a proper tax return will have gone in anyway

HMRC is never going to accept this as payment in a million years and, as we have seen, no court is going to tell them they have to.

There will never be a credit for this ‘payment’.

As such, it will be simply the fact that the taxpayer has not paid the tax that has been assessed. It is not illegal to owe funds to HMRC. However, unsurprisingly, they will expect you to pay, make attempts to enforce and collect the debt, and, ultimately, take you through the civil courts.

It will be tax, interest and, depending on the tax, late payment penalties plus costs.

I am aware of at least one person who entered this ‘planning’ for dealing with SDLT planning and is now being chased vigorously by HMRC.

Of course, like other Sovereign Citizen plays, the response will be that this is part of the playbook. ‘Obstacles are expected.’ ‘You don’t expect them to allow you to draw your magic money on your secret magic trust without a fight do you?’

As such, it would be the client who has found themselves under the spell of the Magic Beans who would consider what actions in law they could take against this confidence trick.

The Fraggles and that protonic reversal I mentioned

So, this brings me to the denouement and the crossing of those proton streams.

The Fraggles, who make up in chutzpah what they lack in legal sanity, meet recruitment agencies. The agencies work with, and place workers through, umbrella companies.

The umbrella industry has its many, many battle scars over the years. Many self-inflicted.

But it is still one where a good number of its participants – including agents and brolly providers – who want to wring every last penny out of it. Especially ahead of what appear to be huge changes from April 2026 (when allied to the broad definition of ‘participator in employment arrangements’ as part of the Employment Rights Bill).

In some shape or form, the plan is to use magic beans to pay VAT and / or PAYE liabilities.

Now, having some experience in dealing with some of these entities who have got themselves in a pickle over VAT and PAYE, I cannot imagine it will be long before HMRC Fraud Investigation Services takes an interest in any such business trying to pay its liabilities in Beans. And a pretty bloodthirsty interest.

It is the perfect storm. Or, if you prefer, protonic reversal.

What’s more, bearing in mind the proliferation of ‘facilitation’ type provisions that are now in play, anyone in that chain who has knowledge of this madness is likely to find themselves in deep Doozer doo-doo.

Conclusion

Dance your cares away?

Well, when it comes to paying tax liabilities, you might find trying to settle with HMRC through the medium of dance more successful than trying to use these Bills of Exchange.

I would suggest that anyone, when confronted by someone selling these Magic Beans, steers a course well clear of this particular magic bean covered rock.

If you run aground, it’s unlikely that it will be one of those cuddly Fraggles waiting to greet you.

[1] Though, with my aptitude for dancing, perhaps not!

[2] I appreciate there is a slight 80s whiff to my cultural references.

[3] Well, not totally.

[4] https://www.canlii.org/en/ab/abqb/doc/2012/2012abqb571/2012abqb571.html

[5] Meads v. Meads, 2012 ABQB 571

[6] For completeness, OPCA stands for Organised Pseudolegal Commercial Argument

[7] From [Fraggle Rock’s] own documents

[8] From [Fraggle Rock’s] own documents

[9] From [Fraggle Rock’s] own documents

[10] From [Fraggle Rock’s] own documents

[11] Consumer notice: WeRe Bank | FCA

[12] Happy to be corrected on this