An opening confession

I confess. I have a bad habit.

I will liberally use “clearly” and “obviously” when explaining tax.

The thing with UK tax is that these are liberties one shouldn’t take. I mentioned this in an old article – “how to make a peanut butter and banana sandwich”.

But some things are obviously so obvious that they don’t need explaining? Right?

Wrong.

About 18 months ago, a client of mine, a property developer, was looking to buy a new site.

He was approached by a firm who promised to make his SDLT liabilities, effectively, disappear.

Understandably, perhaps, my client was interested in exploring. He ran this idea past me.

Usually, you get some idea of a series of transactions or an argument that leads to a client having a ‘filing position’. In other words, some kind of basis (of varying degrees of merit!) on which to file a tax return reflecting a saving.

But not here.

I opened up the attachment and, firstly, was faced with a rather agricultural looking document. But presentation isn’t everything, right?

So what was the deal?

Yeah, what is the deal?

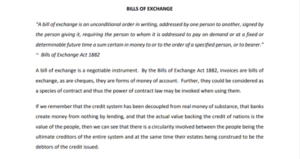

Broadly speaking, it is that ‘bills of exchange’ can be used to settle liabilities of all kind – including taxes.

But aren’t bills of exchange a posh name for cheques?

Well, let me tell you a story. Actually, I’ll let TreasuryDirect, a US Gov website, tell you the ‘story’ which is as follows:

When the United States went off the gold standard in 1933, the federal government somehow went bankrupt.

With the help of the Federal Reserve Bank, the government converted the bodies of its citizens into capital value, supposedly by trading the birth certificates of U.S. citizens on the open market.

After following a complicated process of filing UCC documents with either the Secretary of State of the person’s residence or another state that will accept the filings, each citizen is entitled to redeem his or her “value” by filling out a sight draft drawn on their (non-existent) TreasuryDirect account.

The scheme asserts that each citizen’s Social Security Number is also his or her account number.

As a part of the scheme, participants also file false IRS Forms 8300 and Currency Transaction Reports in the name of law enforcement officials and other individuals they seek to harass.

…

With early and vigorous prosecution by the Justice Department on bogus Sight Draft cases, we have begun to see Bills of Exchange taking their place.

This change occurred on or around January 2001.

All these Bills of Exchange drawn on the U.S. Treasury are worthless.

All the same issues and background materials applicable to Sight Drafts also apply to Bills of Exchange.

This is the same fraud under another name[1].

But that’s the US. They have maple syrup on bacon. It couldn’t happen in the UK?

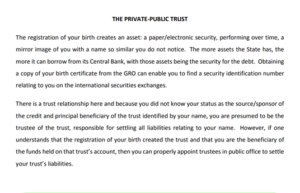

Well, the scheme I am talking about is essentially the UK version, with one or two tweaks:

As we can see, this version of the story suggests that your birth creates a fund held by the state that one can dip in and out of(!)

Lo and behold, the Treasury dismissed this[2] barmy idea back in 2019.

Next, we get the spiel on bills of exchange:

But, hold your horses.

We then have some legal authority for this plan thrown in our faces. From the indomitable Lord Denning no less:

We can’t argue with Denning, surely.

But its difficult to see how a quote could be taken any more out of context than this.

The quote is used to demonstrate some judicial authority that the ‘cheque’ is to be treated as if it is cash. As such, the recipient must accept it in settlement of the debt.

But, of course, this isn’t what he was saying.

In fact, it is averred, Lord Denning was saying precisely the opposite.

What he was saying in that passage is that if a debtor provides a bill of exchange or a promissory note to a creditor, it is binding on the debtor. In other words, the debtor (person making out the cheque) must honour the cheque unless there is a good reason why not.

Importantly, a bill of exchange will only extinguish an existing debt if the creditor agrees with that mechanism of payment. Of course, a creditor is always entitled to insist on payment in legal tender.

A creditor need no more accept a bill of exchange than he or she must accept a payment in magic beans.

So, what does the promoter say about the position if the creditor refuses?

Well that’s handy. If they refuse it, they are accepting it.

Check mate, creditor.

Of course, this is bobbins.

Indeed, this is something that was considered by the Financial Ombudsman in a complaint by mortgage holders who tried to settle a mortgage with bills of exchange from a bank, which wasn’t really a bank, called WeRe Bank.

Additionally, the FCA issued an alert against WeRe Bank back in 2015[3].

Back to tax?

So, what has this got to do with tax?

Well, as I say, the first time I came across this yarn was through a person shilling it to one of my clients in order to ‘help’ him pay his SDLT liability.

However, over the weekend just past I came across it again. The advice being simple. Create a BOE – that draws on this magic and secret fund held by the treasury – and use it to pay your tax liability.

If they don’t respond… they’ve accepted.

If they reject it, then even better!

Certainly, if the spiel is to be believed, it seems to be being offered to quite a few individuals and companies with SDLT, and other, tax liabilities.

This takes me back to the original point and “obviously”.

I assume that the two people who might read this article will be professional advisers. The scheme outlined appears so ‘obviously’ daft that we think our clients won’t fall for it.

But, even if something sounds too good…

…or too barmy…

… can you really be so sure that a client doesn’t want to believe it’s true?

Conclusion

In my opinion, the only thing that is likely to save the client from charges of fraud here is that:

- It is so ludicrous that HMRC will be too busy laughing to send the skin peelers around; and

- It seems that a proper tax return will have gone in anyway – so the dispute is over the form of payment

So tax and interest and late payment penalties (if applicable) seem to be the order of the day.

Indeed, the fact that the proper (SDLT, in this case) return will have gone in is also puzzling commercially.

HMRC is never going to accept this as payment in a million years and, as we have seen, no court is going to tell them they have to. There will never be a credit for this payment on the account.

As such, bearing in mind that it seems the proposal is for a partly contingent fee, how does the promoter ever get fully paid?

Maybe the initial fee is all they plan to take?

Magic beans anyone?

[1] Note there is also an interesting (in a dull sense) here: https://www.youtube.com/watch?si=hhOCGsS85VxbXa_v&v=sICp–cDyr0&feature=youtu.be

[2] https://www.gov.uk/government/publications/paying-debts-using-a-national-insurance-number-or-birth-certificate/paying-debts-using-a-national-insurance-number-or-birth-certificate

[3] https://www.fca.org.uk/news/news-stories/consumer-notice-were-bank